If you’re struggling with debt, you’re not alone. Millions of people in the U.S. face the same challenge, and many wonder how to pay off debt faster. Whether it’s credit card debt, student loans, or a mortgage, paying off debt faster is a goal that seems tough but is entirely achievable. The key is understanding the proven strategies that can help you make a significant dent in your debt.

By following the right methods, you can reduce interest payments, boost your savings, and achieve financial freedom more quickly. In this article, we will walk you through actionable steps that have helped countless individuals pay off debt faster and regain control of their finances.

Why Paying Off Debt Faster Matters

The sooner you pay off debt, the sooner you’ll regain financial control. Not only will you reduce your financial stress, but you’ll also avoid paying more in interest, allowing you to allocate more money toward savings and investments.

Impact on Mental and Emotional Health

Debt can cause significant stress. Constant worry about paying bills, dealing with collectors, or managing high-interest rates can negatively affect your mental health. By eliminating debt, you will gain peace of mind and a sense of financial freedom.

Financial Freedom

Once your debts are cleared, you’ll have more income to put toward savings, investments, or other financial goals. No more monthly payments going to creditors—just extra cash that can grow your wealth.

Interest Savings

The longer you carry debt, the more you’ll pay in interest. Paying off debt faster reduces the total amount of interest you pay over time. For example, credit card interest rates can easily climb over 20%, so paying it off early will save you hundreds or even thousands of dollars.

Understanding Your Debt

Before you dive into strategies, it’s important to fully understand your debt situation. This step is crucial for creating a well-targeted plan.

How to Assess Your Total Debt

Start by listing all your debts, including credit cards, student loans, and any personal loans. Write down the outstanding balance, interest rates, and minimum payments. Knowing your total debt will help you create an actionable plan.

How to Identify High-Interest Debt

Focus on high-interest debt first, like credit card balances, as they typically cost the most in the long term. Tackle these debts to reduce the amount spent on interest over time.

Top Proven Strategies

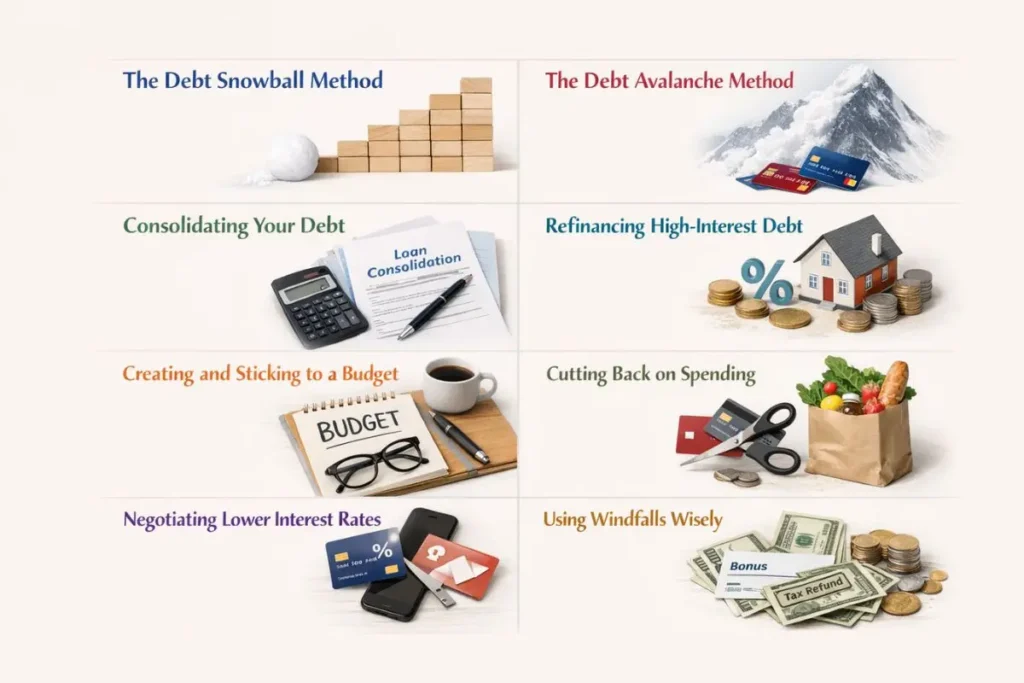

The Debt Snowball Method

The Debt Snowball Method is all about building momentum. Start by paying off the smallest debt first, then move on to the next one. While this method might take a bit longer if you’re working with high-interest debt, the psychological benefits are enormous.

How to implement the Debt Snowball method:

- Step 1: List your debts from smallest to largest.

- Step 2: Focus all your extra money on paying off the smallest debt first while paying minimum payments on the rest.

- Step 3: Once the smallest debt is paid off, move to the next debt on the list and keep building momentum.

Why it works: The quick wins from paying off smaller debts first will motivate you to tackle larger debts. The feeling of accomplishment keeps you moving forward.

The Debt Avalanche Method

The Debt Avalanche Method works by focusing on the debt with the highest interest rates first. This method is great for saving money on interest in the long run, as it reduces the amount of interest you will pay over time.

How to implement the Debt Avalanche method:

- Step 1: List your debts from highest to lowest interest rate.

- Step 2: Put all extra money toward the debt with the highest interest rate.

- Step 3: Once the highest-interest debt is paid off, move to the next one with the highest interest rate.

Why it’s effective: Paying off high-interest debt saves you more money in the long run, reducing the total cost of your debt. For example, credit cards with interest rates above 20% can add up quickly, so eliminating these debts first is a smart move.

Consolidating Your Debt

Debt consolidation involves combining multiple debts into one loan, ideally with a lower interest rate. This can simplify your payments and lower your monthly expenses, making it easier to pay off debt faster.

How consolidation works:

- Take out a loan (usually a personal loan or a balance transfer credit card) to consolidate your debts.

- Use the loan to pay off credit cards, personal loans, or other high-interest debts.

- You only have one payment to manage, and ideally, the interest rate on the new loan will be lower.

Pros of debt consolidation:

- Easier to track with just one payment.

- Lower interest rates could save you money in the long run.

Things to consider:

- Make sure the interest rate is low enough to make it worthwhile.

- Avoid running up more debt after consolidating.

Refinancing High-Interest Debt

Refinancing is another strategy to lower your interest rates. By replacing an old high-interest loan with a new one at a lower rate, you can reduce monthly payments and save on interest.

How to refinance your debt:

- Look for refinancing options, such as consolidating credit card debt into a personal loan with a lower interest rate.

- For mortgages or student loans, refinancing can help secure a lower interest rate.

- Use the savings from the lower interest rate to pay off the loan more quickly.

Why it helps: Refinancing helps you save money by lowering your interest rate, meaning more of your monthly payment goes toward the principal balance. This allows you to pay off the loan faster and save on interest.

Creating and Sticking to a Budget

A well-organized budget is the foundation of successful debt repayment. By creating a budget, you’ll know exactly where your money is going and where you can cut back to free up more cash for debt repayment.

How to create a budget:

- Track your monthly income and expenses.

- Identify areas where you can reduce spending (like dining out or subscription services).

- Allocate the extra money toward paying off debt.

Budgeting tools to consider:

- Mint: A free budgeting tool that helps you track expenses and set financial goals.

- YNAB (You Need a Budget): Helps you plan your spending and save more for debt repayment.

By sticking to a budget, you’ll be able to allocate more money toward your debt, paying it off faster.

Finding Ways to Cut Back on Spending

Sometimes, the quickest way to pay off debt faster is by reducing your monthly expenses. This extra money can then go directly toward debt repayment.

Practical ways to cut spending:

- Cancel subscriptions you don’t use (Netflix, gym memberships, etc.).

- Cook meals at home instead of dining out.

- Use public transportation or carpool instead of owning a car.

Increase your income: Look for opportunities to boost your income through side gigs or freelancing. For example, if you enjoy writing or graphic design, offer your services on freelancing platforms like Upwork or Fiverr.

Negotiating Lower Interest Rates

It’s often overlooked, but you can negotiate with your creditors to reduce your interest rates. If you’ve been a responsible borrower, they may be willing to work with you.

How to negotiate:

- Call your credit card company or lender.

- Ask for a lower interest rate. Mention your good payment history.

- If they’re not willing to lower the rate, consider moving your debt to a balance transfer credit card with 0% APR for a set period.

By negotiating a lower interest rate, more of your payment will go toward the principal balance, which helps you pay off debt faster.

Using Windfalls Wisely

Tax refunds, bonuses, or other unexpected financial windfalls are opportunities to pay down your debt faster. Instead of spending them, use them to reduce your balance.

How to use windfalls:

- Apply tax refunds directly to high-interest debt.

- Use work bonuses or side income to make a lump sum payment.

By using these windfalls wisely, you can pay off a significant portion of your debt in a short amount of time.

Is It Time to Get Professional Help?

Sometimes, managing debt on your own can feel overwhelming. If you’re struggling, professional help might be necessary.

When to seek credit counseling: If you find it difficult to manage multiple debts, a credit counselor can help you create a structured plan.

Debt management programs: These programs can help you negotiate with creditors and reduce your monthly payments.

Debt settlement: As a last resort, this can help you settle debts for less than what you owe, but it may impact your credit score.

The Role of Emergency Funds

While paying off debt, it’s still important to save for unexpected expenses. Building a small emergency fund ensures you don’t fall back into debt if something unexpected happens.

How to balance saving and paying off debt:

- Start with a small emergency fund (aim for $500-$1,000).

- Once your emergency fund is in place, redirect savings toward debt repayment.

Having an emergency fund helps prevent adding to your debt while you pay it off.

How to Avoid Falling Back Into Debt

Paying off debt is a great accomplishment, but it’s important to avoid falling into the same trap again.

How to maintain a debt-free lifestyle:

- Establish good financial habits, such as budgeting and saving regularly.

- Build and maintain good credit to prevent future reliance on credit cards or loans.

- Stick to a savings plan to ensure you’re prepared for emergencies without using credit.

Success Stories and Case Studies

Hearing real-life examples can be encouraging. Many people have successfully used these strategies to pay off debt faster.

Example:

- Sarah, a teacher in Texas, used the Debt Snowball method to pay off $15,000 in credit card debt in two years. By paying off smaller debts first, she stayed motivated and made steady progress.

Testimonial:

- “I was overwhelmed with student loans, but after refinancing and sticking to a strict budget, I paid off my debt 3 years earlier than expected,” says John, a 28-year-old software developer in California.