Credit cards, when used correctly, can be a powerful tool for managing your finances and building a strong credit history. However, how to use credit cards responsibly is crucial to ensure that you avoid the dangerous pitfalls of debt traps. Many people unknowingly find themselves trapped in credit card debt, leading to financial stress and a damaged credit score. Understanding the importance of responsible usage can help you reap the benefits of credit cards, such as earning rewards and increasing your purchasing power, without falling into debt traps.

This guide will walk you through the essential steps of managing credit cards responsibly, including tips to avoid overspending, keeping track of balances, and maintaining a good credit score. By following these strategies, you can use credit cards wisely, improve your financial health, and steer clear of the traps that can derail your financial future.

What is Its Usage?

Responsible credit card usage refers to using your card in a way that helps build your credit while avoiding excessive debt. By paying off balances on time and not exceeding your credit limit, you can enjoy the benefits of your card without falling into financial difficulty.

Here are the key principles of responsible credit card usage:

- Pay your balance in full every month: This avoids interest charges.

- Stay within your credit limit: Avoid exceeding your credit limit to prevent penalties.

- Be selective about your purchases: Don’t use credit for things you can’t afford to pay off immediately.

When you follow these steps, your credit card works for you instead of against you.

Risks of Not Using

Failing to use your credit card responsibly can quickly lead to debt traps. When credit cards are misused, it results in higher balances and interest charges. Here’s a breakdown of the potential risks:

- Late payments: Missing a payment can result in hefty late fees, a higher interest rate, and damage to your credit score.

- Paying only the minimum payment: If you only pay the minimum, it can take years to pay off your balance, with interest accumulating during that time.

- Maxing out your credit card: This can hurt your credit score and put you in a cycle of debt that’s hard to break.

The credit card debt cycle can spiral out of control if you don’t keep a close eye on your spending and payment habits.

How Credit Card Debt Traps Are Formed

Debt traps form when you continue to charge purchases to your card without paying off the balance. The main factors contributing to this are:

- Interest accumulation: Credit cards often have high interest rates (APR). If you carry a balance, the interest starts to pile up, making it even harder to pay off the debt.

- Late fees: Missing a payment adds fees on top of your existing balance, which then accrues even more interest.

For example, let’s say you have a $500 balance on your card with a 20% APR. If you only make the minimum payment of $25 a month, it will take years to pay off the debt—and you’ll end up paying far more than $500 due to interest.

Tips for Using

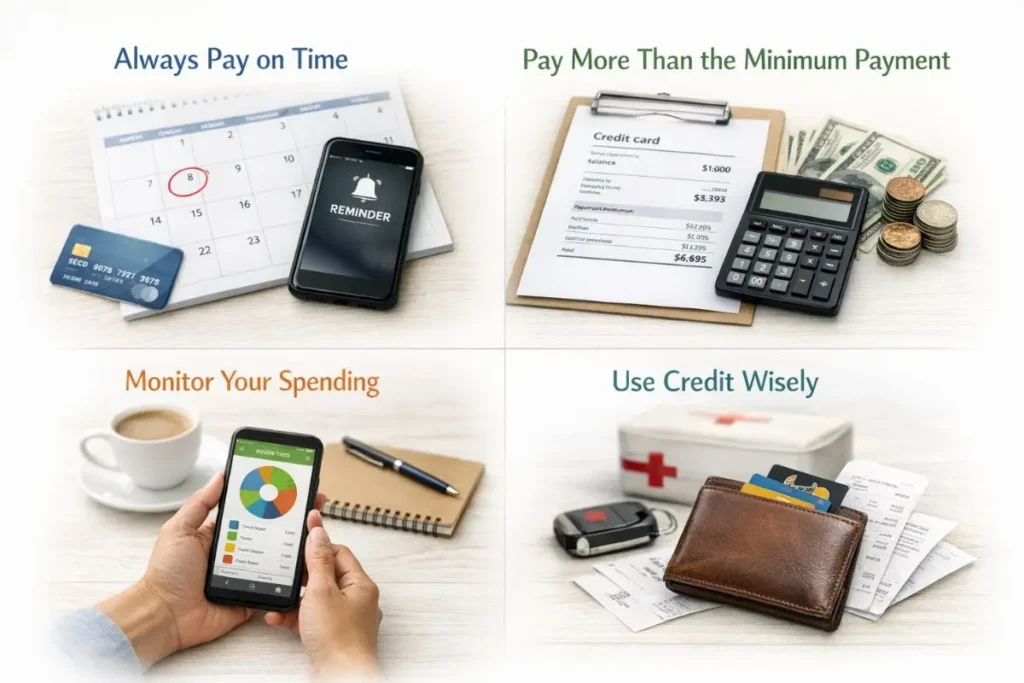

Always Pay on Time

One of the easiest ways to use credit cards responsibly is to make sure you pay your bill on time every month. When you miss payments, you incur late fees and your interest rate may increase, which makes it even harder to pay off your debt. You can avoid this by setting up automatic payments or setting reminders on your phone.

Pay More Than the Minimum Payment

Paying only the minimum can seem like a good option because the payment amount is small. However, paying only the minimum allows interest to build, making your debt harder to pay off. Try to pay more than the minimum each month to reduce your balance faster. This will save you money on interest over time.

Monitor Your Spending

Keep track of your spending and ensure you’re not charging more than you can afford to pay off. Use budgeting apps or create a monthly spending plan to avoid overusing your credit card. Being mindful of your expenses ensures you don’t exceed your budget and stay out of debt.

Use Credit Wisely, Not as a Substitute for Income

A credit card should never be used to cover regular expenses or as a way to make ends meet. If you find yourself using credit for basic needs, it’s time to reassess your financial situation and make adjustments. Credit cards should be used for planned purchases or emergencies, not as a way to spend beyond your means.

Creating a Budget to Stay on Track

A solid budget can help you control your credit card spending. Here’s how to create one:

- Track your income: Know how much you’re earning each month.

- List your expenses: Include all monthly expenses like rent, groceries, and utilities.

- Set limits: Allocate a specific amount for credit card purchases.

- Review your budget regularly: Check your budget every month to make sure you’re staying on track.

With a budget in place, you’ll have a clearer picture of where your money is going and how to stay within your spending limits.

How to Avoid Traps

Avoiding debt traps requires a few strategies:

- Use credit cards for emergencies: Avoid charging non-essential items to your card.

- Keep track of your credit limit: Never exceed 30% of your limit to avoid damaging your credit score.

- Choose credit cards with rewards: Some cards offer rewards for responsible spending, but make sure you’re not spending just to earn them.

By using these strategies, you can stay in control of your credit card usage and avoid debt traps.

Transfer Your Balance to Lower Interest Cards

If you’re struggling with high-interest debt, consider transferring your balance to a card with a lower interest rate. This could help you save on interest and pay off your debt faster. However, be careful about balance transfer fees, which can negate any savings from the lower APR.

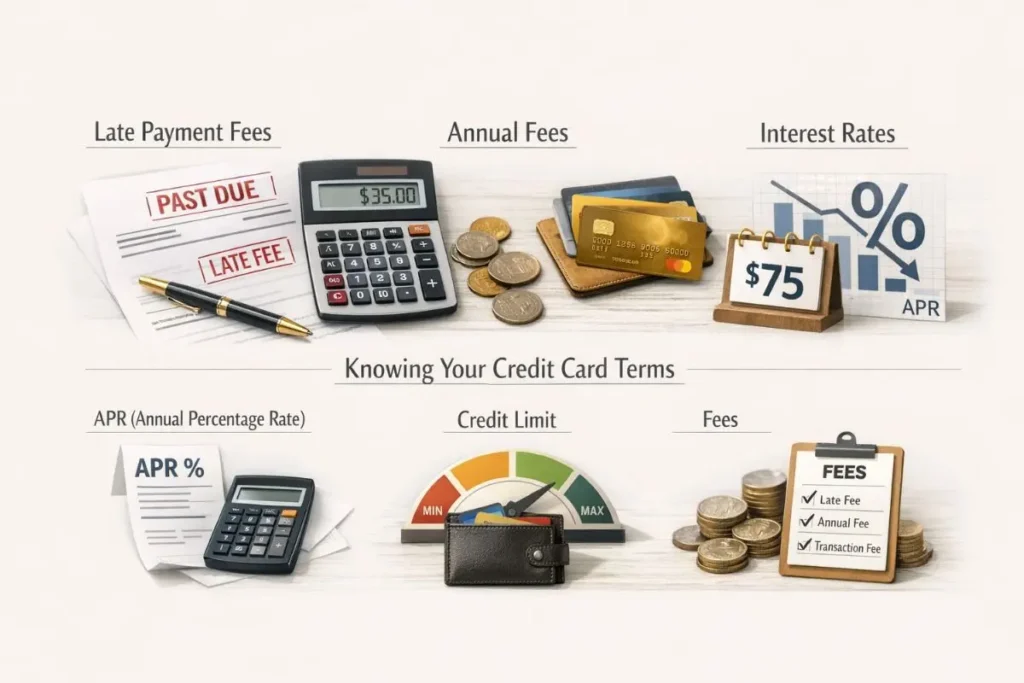

Credit Card Fees and Interest Rates

Credit cards come with various fees and interest rates that can add up quickly. Here’s what you need to know:

- Late payment fees: These can be as high as $35 per missed payment.

- Annual fees: Some cards charge yearly fees, often ranging from $25 to $100.

- Interest rates: The average APR on credit cards is around 16%, but this can vary greatly.

Before applying for a credit card, make sure to read the fine print and understand the associated fees and rates. This will help you avoid unexpected costs.

Knowing Your Credit Card Terms

Every credit card comes with terms and conditions that you should be aware of:

- APR (Annual Percentage Rate): This is the interest rate you’ll pay on your balance if you don’t pay it off in full each month.

- Credit limit: The maximum amount you can charge to your card.

- Fees: Late fees, annual fees, and transaction fees can all add to your costs.

Make sure you understand all of these terms before using your card. This will help you make informed decisions and avoid credit card debt.

Trapped in Debt? Escape Now!

If you’re already in credit card debt, here are the steps to take:

- Stop using your card: Cut back on spending and focus on paying off your balance.

- Contact your card issuer: You may be able to negotiate lower interest rates or extend your payment terms.

- Consider debt consolidation: Combine multiple credit card debts into one manageable payment with a lower interest rate.

If your debt is too overwhelming, seeking help from a credit counselor can help you explore your options.

Seek Professional Help if Needed

If you’re struggling to manage credit card debt, reaching out to a financial advisor or credit counselor can provide guidance. These professionals can help you create a plan to pay off your debt and improve your financial situation.

Power of Credit Scores in Credit Card Management

Your credit score is a reflection of how responsibly you use credit. It impacts your ability to qualify for loans, mortgages, and more. Here’s how to maintain a good credit score:

- Pay bills on time: Your payment history is the largest factor affecting your score.

- Keep your balance low: Aim to keep your balance under 30% of your credit limit.

- Check your credit report: Review your credit report annually to catch any errors.

How Credit Card Usage Affects Your Credit Score

The way you use your credit card directly impacts your credit score. Factors include:

- Payment history: On-time payments boost your score.

- Credit utilization: Keeping your balance low relative to your credit limit helps improve your score.

- Length of credit history: The longer you’ve had credit, the better.

By practicing responsible credit card usage, you can build and maintain a strong credit score.