Buying a home is a significant milestone, but it requires careful planning, especially when it comes to saving for a home down payment. Setting up a budget is the first and most important step in this journey. It helps you track your progress and ensure that you’re saving enough for the down payment while managing other financial responsibilities. By understanding how much you need, creating a realistic savings plan, and cutting unnecessary expenses, you can make your dream home a reality. In this guide, we’ll explore the best strategies to set up a budget, manage debt, and save effectively to help you reach your down payment goal.

Why Setting Up a Budget is Crucial for Saving

A solid budget isn’t just about keeping track of your money; it’s the foundation of your journey toward homeownership. Without a proper plan, it can be difficult to save for a home, which is often one of the largest expenses when purchasing a house.

Key Points to Remember:

- Tracking savings: A budget helps you monitor your progress and keep your eye on the prize.

- Realistic expectations: Understanding how much you need to save helps you set realistic, achievable goals.

- Smart financial decisions: A well-thought-out budget allows you to manage both short-term expenses and long-term savings.

Creating and sticking to a budget ensures that you’re financially prepared to make the down payment and cover the costs of buying a home.

Understanding the Importance

A down payment is the initial sum of money you pay when purchasing a home, typically a percentage of the home’s total price. While the exact amount can vary depending on the type of loan, a larger down payment can have a significant impact on your mortgage terms.

Benefits of a Larger Down Payment

- Lower monthly payments: A bigger down payment means you’re borrowing less, which translates to lower monthly mortgage payments.

- Better mortgage rates: Lenders tend to offer better interest rates to borrowers who can afford a larger down payment, saving you money in the long run.

- Avoiding private mortgage insurance (PMI): If you put down 20% or more, you can often avoid the extra cost of PMI, which is required if your down payment is below 20%.

Steps to Set Up a Budget

- Assess your current financial situation: Take a detailed look at your income, spending habits, and existing savings.

- Calculate your down payment goal: Use a home price calculator to estimate how much you’ll need to save based on the homes you’re interested in.

- Identify sources of income and savings: This might include your salary, freelance income, or any side jobs you have. You should also check if there are any funds that can be redirected into your down payment savings.

- Track your expenses: Categorize your spending to find areas where you can cut back—whether that’s limiting takeout or subscription services.

- Set up a monthly savings target: With your financial picture clear, decide how much you can save each month and start working toward that goal.

Best Strategies to Save

- Open a separate savings account: Keep payment savings separate from your regular checking account to avoid spending it on other things.

- Explore high-yield savings accounts: These accounts offer better interest rates than regular savings accounts, helping your savings grow faster.

- Reduce unnecessary spending: Cut back on non-essential expenses like dining out, entertainment, or luxury purchases.

- Automate savings: Set up automatic transfers to your savings account each payday to ensure you’re consistently putting money aside.

- Use windfalls: Tax refunds, work bonuses, or other unexpected cash inflows can be used to boost your savings.

By incorporating these strategies into your routine, you can maximize the amount of money you’re saving for your down payment.

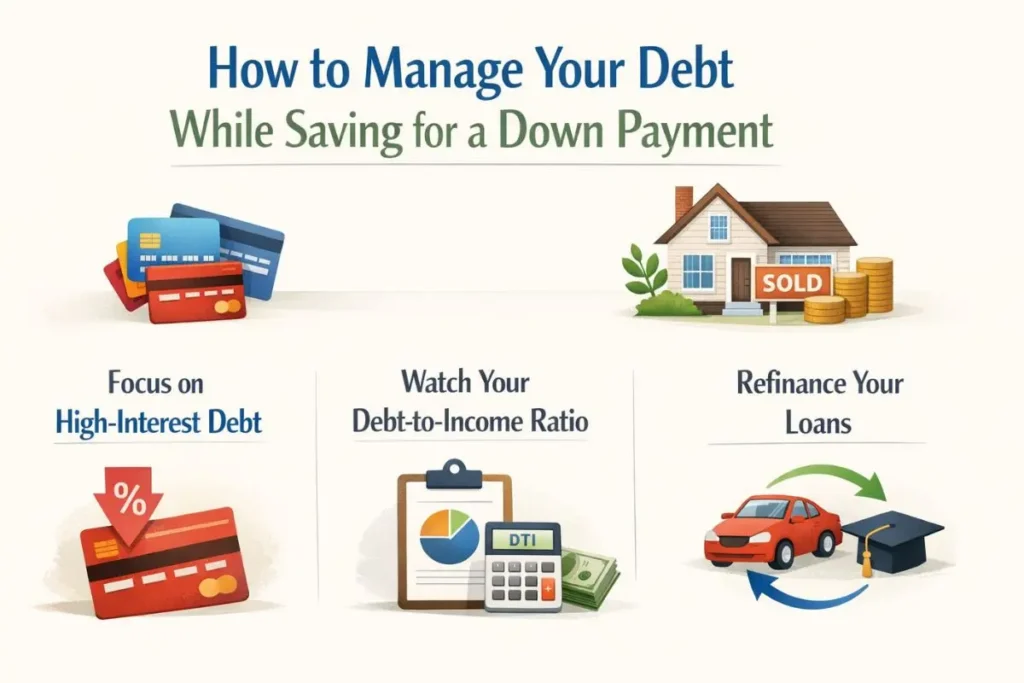

How to Manage Your Debt While Saving

- Focus on high-interest debt: Prioritize paying off high-interest debt (credit cards, payday loans) before focusing on savings.

- Debt-to-income ratio: Keep an eye on your debt-to-income ratio (DTI), which is an important factor for mortgage approval. The lower your DTI, the better your chances of securing a mortgage with favorable terms.

- Refinance loans: Refinancing high-interest loans like student loans or car loans can lower your monthly payments, freeing up more money for savings.

By reducing debt and improving your financial profile, you’ll be in a stronger position to save for your home down payment.

Exploring Assistance Programs

In some cases, saving for a home might feel like an insurmountable task. Luckily, there are several down payment assistance programs available for first-time buyers.

Types of Assistance:

- Grants: Some local and state governments offer non-repayable grants to help with down payments.

- Low-interest loans: Certain programs provide loans with low or zero interest rates, which can be paid off later.

- Deferred loans: These loans are deferred until you sell your home or pay off your mortgage, making them an attractive option for first-time homebuyers.

Check with local housing authorities, banks, and other institutions to find out which programs you qualify for.

How to Overcome Challenges

Even with the best planning, saving for a home can come with its challenges. Whether it’s an unexpected medical bill or a temporary drop in income, life has a way of throwing curveballs.

Common Challenges:

- Unexpected expenses: Car repairs, medical bills, or other emergencies can derail your savings plan.

- Income fluctuations: If your income varies month-to-month, you may find it difficult to keep your savings consistent.

Solutions to Overcome These Challenges:

- Build an emergency fund: This helps cover unexpected costs without dipping into your down payment savings.

- Stay flexible: If something unexpected comes up, adjust your budget and make up for the missed savings later.

By staying disciplined and planning for the unexpected, you can stay on track to meet your down payment goal.

Making Adjustments to Your Budget

Your financial situation will likely change as you save and your budget will need to adjust accordingly.

How to Make Adjustments:

- Increase savings after paying off debt: Once you’ve paid off a loan or credit card, direct that money into your savings.

- Adapt to life changes: If your income changes, revise your savings plan to account for the shift.

- Prioritize big savings months: If you get a tax refund or a bonus at work, allocate that money to your down payment fund.

This flexibility ensures that you can stay on course even as circumstances change.

What to Do Once You Have Enough

Once you’ve saved enough for your down payment, the real fun begins—buying your home! But before you start house-hunting, here are some essential steps.

Key Steps:

- Get pre-approved for a mortgage: This gives you an idea of how much home you can afford and helps streamline the home-buying process.

- Start house hunting: With your pre-approval and down payment ready, you’re in a strong position to begin finding your dream home.

- Account for closing costs: Don’t forget about the additional fees like inspection costs, legal fees, and title insurance, which typically amount to 2-5% of the purchase price.

FAQS

1. How much should I save for a down payment on a house?

- Generally, aim for 20% of the home’s purchase price. However, there are programs available that allow down payments as low as 3% to 5%.

2. How do I start saving for a home down payment?

- Begin by assessing your financial situation, setting a realistic savings goal, creating a budget, and opening a dedicated savings account. Automate your savings to stay on track.

3. Can I buy a house with no down payment?

- Yes, there are VA loans (for veterans) and USDA loans (for rural buyers) that allow no down payment. These loans have specific eligibility requirements.

4. What are the best strategies to save for a home down payment?

- Set up a high-yield savings account, automate your savings, cut back on unnecessary expenses, and use any windfalls like tax refunds or bonuses to boost your savings.